Executive summary

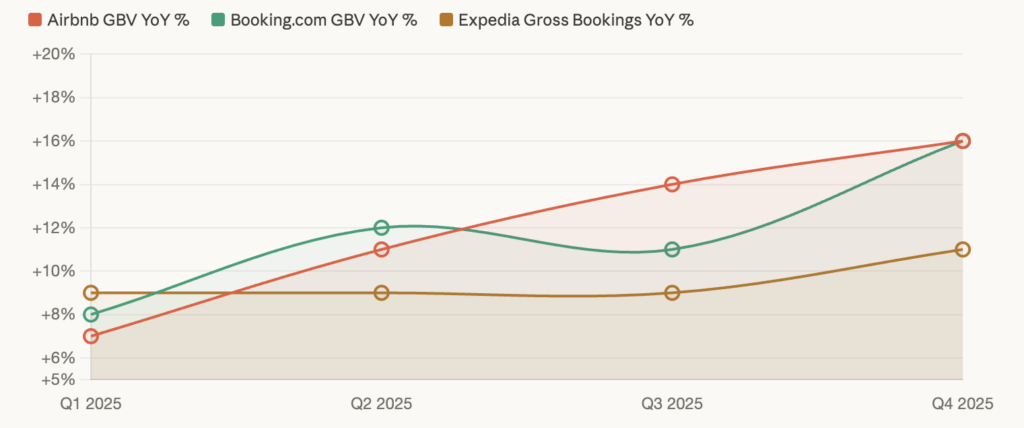

- All three major OTAs closed Q4 2025 with their strongest quarter of the year, each posting room night growth of 9–10% and gross booking value growth of 13–16% year over year.

- The U.S. market staged a notable comeback — Booking.com accelerated from low single-digit growth in H1 to low double-digits in Q4, while Airbnb reached mid-single digit growth in North America, its strongest regional performance of the year.

- AI moved from strategy slide to P&L line item: Booking.com reported a 10% reduction in customer service cost per booking directly attributable to generative AI, while Airbnb disclosed that its AI assistant is now resolving about a third of all issues without needing a live agent.

- Short-term rental supply continues to expand across all three platforms — Airbnb surpassed 9 million active listings, Booking.com’s alternative accommodation inventory grew 8% to 8.6 million, and Expedia grew its total lodging property count by more than 10%.

Travel demand carried its momentum into year-end with conviction. The question heading into Q4 2025 earnings season was whether platforms could sustain the pace they set through summer, against tough prior-year comparisons and a consumer base in the U.S. still exercising some caution on discretionary spending. The answer, across Airbnb, Booking.com, and Expedia, was a qualified yes — with Q4 becoming each platform’s strongest quarter of the year.

What makes this quarter particularly meaningful for property managers is where the growth came from. It wasn’t a single tailwind. It reflected the cumulative effect of product investments — payment flexibility, cancellation policy updates, simplified fee structures — along with genuine acceleration in markets that had previously lagged. The platforms are also converging on a common strategic direction: deepening direct relationships with travelers, deploying AI in ways that generate measurable efficiency gains, and expanding the types of inventory they surface. Each of those moves carries real implications for how professional hosts and property management companies (PMCs) position their portfolios in 2026.

Q4 2025 at a glance

Platform performance was closely clustered at the top line. Room nights grew 10% at Airbnb (its best quarter of the year), 10% at Booking.com (which beat the high end of its own guidance by three percentage points), and 9% at Expedia across hotels and STRs. GBV told a more varied story: Airbnb’s 16% growth was its best in more than two years, Booking.com matched that figure, and Expedia’s lodging gross bookings grew 13.5%.

Booking windows extended across the board relative to 2024. Longer lead times, combined with stronger-than-expected demand late in the quarter, were cited repeatedly as drivers of the room night outperformance. Airbnb’s CFO Ellie Mertz noted that Reserve Now, Pay Later (launched in the U.S. and generating over 70% adoption by eligible bookings in Q4) directly contributed to longer booking windows and a mix shift toward larger, higher-priced homes, which in turn supported ADR growth.

Airbnb: product-led reacceleration

The story at Airbnb in Q4 was one of compounding product improvements showing up in the numbers. Mertz disclosed that three specific product updates, by the company’s own estimate, delivered over 200 basis points of nights growth and roughly 300 basis points of GBV growth: Reserve Now, Pay Later, updated cancellation policies that introduced a 24-hour grace period for shorter stays, and the early stages of a simplified fee structure migrating PMS-connected hosts to a unified 15.5% service fee.

That last item is worth particular attention for property managers using channel management software. Airbnb completed its migration of PMS-connected hosts to a unified 15.5% service fee in Q4, and is now piloting a further migration for individual hosts in select countries.

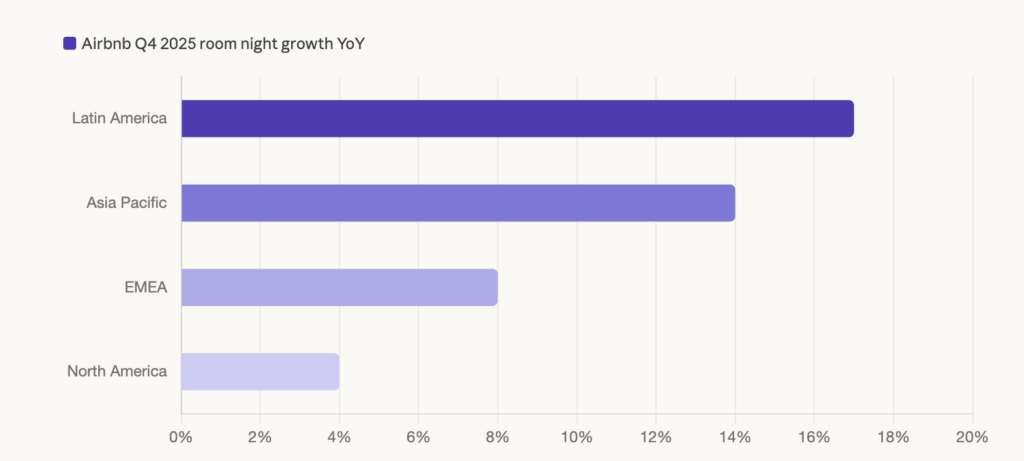

Geographically, Latin America led at high-teens growth, Asia Pacific came in at mid-teens, EMEA at high-single digits, and North America at mid-single digits. India was singled out as a breakout market, with nights booked on an origin basis up 50% year over year and first-time bookers up more than 60%. Brazil, now a top-five market, was Q4’s second-largest contributor of first-time bookers behind only the U.S.

On the product side, Airbnb’s hotel pilot — initially concentrated in boutique and independent properties across New York, Los Angeles, Madrid, and San Francisco — is small but deliberate. As of Q4, hotels represented a single-digit percentage of total nights booked but were growing at nearly double the platform’s overall rate. Airbnb has signaled it plans to expand hotel supply through 2026, with the category expected to represent a meaningfully larger share by year-end. For PMCs properties in supply-constrained urban markets, this expansion could affect competitive positioning in search results.

Booking.com: U.S. acceleration and the scale of Connected Trip

Booking.com’s Q4 was defined by U.S. momentum and the continued maturation of its multi-vertical strategy. U.S. room nights (spanning hotels. STRs, and alternative accommodations) reached low double-digit growth in Q4, up from low single-digits in the first half of the year — an acceleration Booking.com attributed to targeted investments in brand marketing, performance channels, and its B2B business.

Even as volume grew, Booking.com noted that some consumer segments in the U.S. showed slightly lower ADRs and shorter lengths of stay compared to prior-year periods — consistent with continued thoughtfulness around discretionary spending in certain segments. For hosts, this is a dynamic that favors well-reviewed, quality-differentiated properties positioned to earn bookings on merit rather than availability alone.

The Genius loyalty program continues to serve as Booking.com’s clearest differentiator. Level 2 and 3 Genius travelers — now representing a high 50% share of total room nights, up from the mid-50% range in 2024 — book more frequently, book further in advance, and return more consistently than non-Genius travelers. These higher-tier members also have a meaningfully higher direct booking rate, which connects loyalty directly to Booking.com’s channel mix strategy: its B2C direct mix held at mid-60% for the full year.

Boost your short term rentals today

The Connected Trip vision is translating into real transaction volume. For the full year, transactions involving more than one travel vertical grew in the high-20% range and now represent a low double-digit percentage of total transactions. Airline tickets booked across Booking.com’s platforms reached 68 million for the year, up 37%, while attraction tickets grew nearly 80%. The strategic implication for independent property managers is significant: Booking.com’s internal data shows that travelers who book more than one vertical come back more frequently, which means the platform’s investment in Connected Trip is simultaneously deepening traveler loyalty to Booking.com and increasing the relative value of the properties that appear within those itineraries.

Expedia: Vrbo’s return and the B2B engine

Expedia entered 2025 needing to prove Vrbo could grow again after extended headwinds, and Q4 capped a year of recovery. Vrbo delivered its third consecutive quarter of growth, supported by the expansion of VrboCare — a trust and assurance product that CEO Ariane Gorin credited with sharpening the brand’s differentiation — and multi-unit inventory added in late 2024 that now accounts for roughly a third of Vrbo’s growth.

EMEA was the geographic standout, with room night growth reaching low double digits in Q4. ADR across both hotels and short-term rentals rose 4% to $207, with both longer booking windows and longer lengths of stay relative to 2024 contributing to pricing strength. Asia-Pacific growth reflected the impact of geopolitical conditions across several markets.

On supply, Expedia grew its total lodging property count by more than 10% year over year and reported that AI tools have accelerated property onboarding by 70%. Partner-funded promotions reached over 30% of total bookings in Q4, up more than 10 percentage points from Q3. Promotional participation has become an increasingly effective tool for visibility on the platform — PMCs that haven’t yet explored Expedia’s promotional options may find it worth evaluating as part of their distribution strategy, particularly given the volume of partner-funded demand now flowing through those mechanisms.

What the numbers mean for property managers

Mind the fee structure changes on Airbnb. Airbnb completed its migration of PMS-connected hosts to a unified 15.5% service fee in Q4, and is now piloting a further rollout to individual hosts in select countries. If your channel management software hasn’t been updated to account for this, your effective pricing on Airbnb may not match your intent. In such a case, your listings could be appearing less expensive on Airbnb than on competing channels, potentially leaving revenue on the table. Use Guesty’s channel manager to audit how pricing flows across platforms and ensure your rate strategy is consistent across distribution channels.

Longer booking windows require forward-looking pricing. All three platforms reported booking windows extending relative to 2024, with Reserve Now, Pay Later amplifying this trend on Airbnb. While recent months saw many operators report increasingly short lead times, the major OTAs recorded longer booking windows in Q4, which means your calendar pricing needs to be set further out than it may have been in prior years. Static pricing that isn’t updated regularly will either leave money on the table during demand peaks or result in underpriced inventory filling up early. Guesty PriceOptimizer adjusts rates automatically based on lead time, occupancy pace, and local demand signals, keeping your calendar priced correctly whether guests are booking two weeks or six months out.

U.S. demand is healthy and concentrated in quality. Both Airbnb and Booking.com reported accelerating room night growth in the U.S., with some variation in ADR and length of stay across segments. This reflects a market where volume is strong and guests are engaged, with pricing opportunities concentrated in high-quality, well-positioned listings. For PMCs in North American markets, differentiation through quality and guest experience has become more important than it was during the high-demand years post-pandemic. Properties that consistently earn strong reviews and maintain high listing quality scores will have an advantage in ranking algorithms increasingly shaped by quality signals. Guesty’s performance analytics can help you identify which properties are underperforming quality benchmarks before they lose search visibility.

Loyalty programs are reshaping booking patterns. Booking.com’s high-tier Genius members now account for more than half of all room nights — and they book earlier, more often, and more directly. Expedia grew its loyalty membership by mid-single digits in Q4, with faster growth in Silver tiers and above. Platforms are increasingly routing their best, most reliable travelers through loyalty channels. Ensuring your properties are optimized for visibility within these programs — including Genius eligibility on Booking.com — is no longer optional if you want access to that traveler segment.

AI is reshaping operational expectations, not just search. The AI-based efficiency gains platforms are reporting are already affecting traveler expectations. Booking.com’s 10% reduction in customer service cost per booking, Airbnb’s AI support resolving a third of tickets without a human agent, and Expedia’s record self-service levels all point toward guests who now expect faster, more seamless resolution of issues. For PMCs, AI-powered guest communication is increasingly the standard travelers expect, not a differentiator. Guesty’s ReplyAI handles guest messaging intelligently, reducing manual load while keeping response quality consistent at scale.

Expand your distribution footprint. All three platforms grew their supply bases meaningfully in Q4. Airbnb surpassed 9 million active listings, Booking.com’s alternative accommodation inventory reached 8.6 million, and Expedia grew its total lodging property count by more than 10%. Platforms are actively onboarding new properties, with Expedia reporting AI tools have cut onboarding time by 70%. For PMCs not currently listed across all three, now is a practical moment to evaluate gaps in your distribution. Guesty’s integrations marketplace is a good starting point for identifying which channels are available through your existing setup.