The short-term property rental sector grows daily as homeowners weigh the high turnover of vacation stays against the stability of long-term leases. Short-term renting involves weekly guest rotations, constant inquiries, and regular maintenance. While long-term rentals offer a hands-off approach, the operational trade-offs impact your bottom line. This guide breaks down the revenue potential and management requirements for both models.

TL;DR

- Short-term rentals (STR) can generate significantly higher net profits than long-term leases, though the margin depends on market, occupancy rates, and operating costs.

- You maintain total control over property conditions with frequent inspections between stays.

- Long-term rentals offer stability but lock you into fixed margins for years.

- Automation tools bridge the labor gap between short and long-term models.

- STR allows owners to use their properties for personal visits.

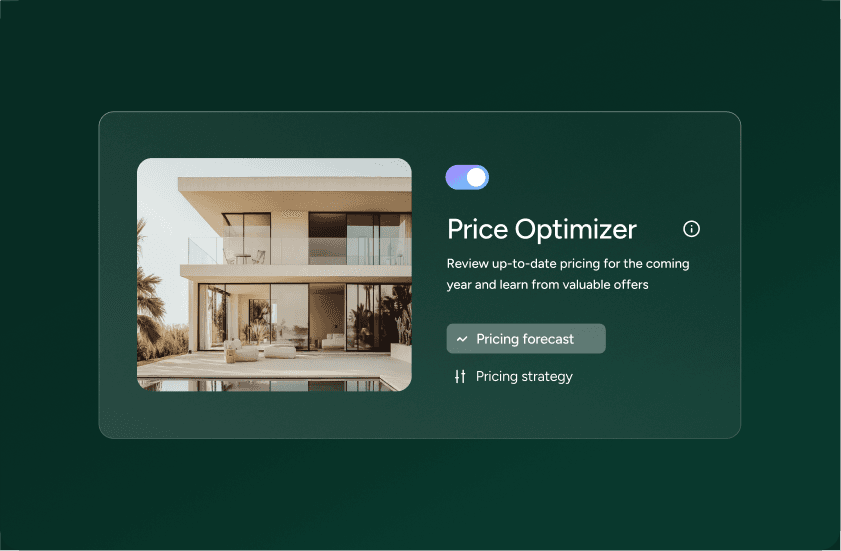

- Successful short-term management relies on closing occupancy gaps through dynamic pricing.

Manage high turnover for higher yield

Short-term rentals involve constant turnover, requiring you to screen guests and approve requests every few days. This frequent cycle means you have less time to build deep relationships with renters, necessitating a different approach to trust. Logistics demand consistent attention to arrange key exchanges, track contact details, and organize calendars to avoid double bookings.

> High turnover keeps your property in peak condition. You catch a leaking faucet on Tuesday instead of discovering a flooded basement six months later during a long-term tenant’s exit.

You must also handle cleaning and maintenance between every visit while stocking essentials like coffee or fresh linens. Fill calendars and protect margins by maintaining high visibility on major booking channels.

Evaluate the hidden costs of long-term rigidity

Committing to one tenant for a year removes the work of constant recruiting but traps you in a binding contract. Finding the right tenant becomes a high-stakes process. A difficult short-term guest is gone in three days. A difficult long-term tenant may take months and legal proceedings to remove. You cannot inspect the premises every week and must entrust the property to others for months or years. Tenants often demand design freedom, which removes your ability to control property aesthetics.

| Feature | Short-term rental (STR) | Long-term rental (LTR) |

|---|---|---|

| Profit margin | High | Low (fixed monthly rate) |

| Operational effort | High (cleaning, messaging) | Low (periodic maintenance) |

| Property control | Total (weekly inspections) | Limited (aAnnual/bi-annual) |

| Flexibility | High (owner can block dates) | None (lease duration) |

| Market resilience | High (dynamic pricing) | Low (locked-in contract) |

Owners often want to visit their properties. Short-term stays allow for this asset access by blocking out a weekend for personal use and profit from guests the rest of the year. Long-term arrangements do not allow this flexibility.

Boost your short term rentals today

Analyze the revenue discrepancy

Earning power serves as the ultimate tiebreaker when comparing models. Long-term rentals represent the wholesale side of real estate, where buying in bulk is cheaper for the tenant but less profitable for the owner. Vacation rental guests pay a premium for convenience and amenities, allowing for significantly higher nightly rates.

Consider the numbers. A property earning $1,000 monthly as a long-term rental might yield $2,500–$3,500 as a short-term rental in a high-demand market. While the revenue premium is significant, it varies by location and seasonality — and the higher operating costs narrow the net margin.

Centralize your communications to manage this workload. Use Guesty Lite™ to sync your multi-calendar and prevent double bookings across platforms.

Close occupancy gaps with technology

Choose short-term renting for higher returns and flexibility. Use technology to handle repetitive tasks like guest interactions, making the workload comparable to long-term leases. Guesty Pro™ triggers messages at check-in and check-out to maintain service levels while protecting your time and increasing revenue.

Guesty scales alongside your portfolio. Use Guesty® Lite™ for 1–3 listings to access the Unified Inbox and essential management tools. For 4 or more units, Guesty Pro™ provides advanced automations and API-integrated tools for complex operations. Guesty Enterprise™ (500+) delivers custom workflows and dedicated support for large-scale operations.

Is short-term rental more profitable than long-term?

Yes. Short-term rentals typically generate significantly higher gross revenue. After accounting for increased utility and cleaning costs, most operators still see meaningfully higher net profit compared to long-term leases.

How do I handle the extra work of short-term rentals?

Use vacation rental management software to automate messaging, calendar syncing, and cleaning schedules. This reduces manual labor to a level comparable with long-term management.

Can I switch my long-term rental to a short-term rental?

Check local zoning laws and HOA regulations first. If allowed, you’ll need to furnish the property, set up accounts on booking channels, and build operational infrastructure for guest communication and cleaning. Some owners transition gradually through mid-term rentals (30+ days) before committing to full STR operations.

What are the main risks of short-term rentals?

The primary risks include seasonal occupancy gaps and potential property damage. You mitigate these through dynamic pricing strategies and guest screening tools.

Does short-term renting affect property wear and tear?

Short-term rentals experience more frequent use of appliances, but they are cleaned and inspected more often. This allows you to identify and fix minor issues before they become expensive repairs.